New AppsFlyer data shows Short Drama emerging as one of the UAE’s fastest-growing subscription categories and a top destination for Android ad spend, signalling a shift in how audiences consume and pay for mobile content

AppsFlyer, the Modern Marketing Cloud, has released its State of Subscriptions for Marketers 2026 report, revealing a sharp shift in consumer behaviour in the Middle East, where the rapid rise of Short Drama apps is reshaping both content consumption and marketing investment strategies.

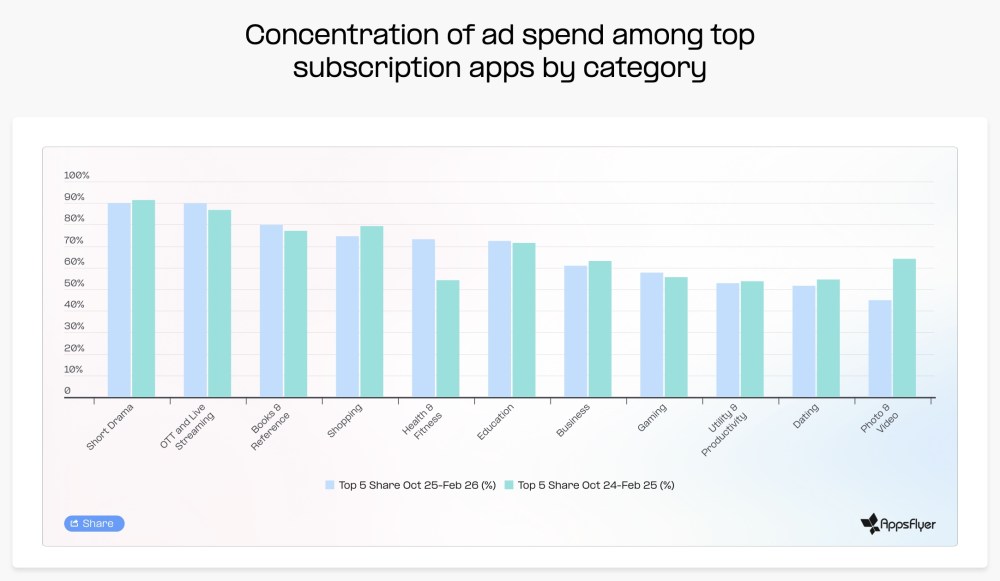

Short Drama, bite-sized, mobile-first serialized video content, is emerging as one of the fastest-growing app categories in the UAE, with installs increasing by 109% year-on-year. Crucially, this growth is not occurring in isolation. The category has quickly become one of the largest recipients of advertising investment, ranking as the second-highest category for ad spend on Android in the Middle East. This alignment between user growth and marketing investment signals a maturing category, where marketers are no longer experimenting, but actively scaling.

The data suggests that this surge is being driven by a fundamental shift in how audiences engage with content. In contrast to traditional long-form streaming, Short Drama is designed for mobile-native consumption, favouring short, episodic formats that lend themselves to frequent engagement. At the same time, discovery within the category is increasingly driven by paid acquisition rather than organic channels, with a growing share of installs attributed to advertising. For marketers, this indicates that success in the category is closely tied to the ability to efficiently acquire users at scale.

Beyond Short Drama, the report highlights how paid user acquisition trends are evolving across subscription app categories in the region, offering insight into where marketers are seeing the strongest returns on investment. Utility and Productivity apps recorded a 491% year-on-year increase in paid installs on Android and a 99% increase on iOS, pointing to strong demand at scale, particularly among Android users. Meanwhile, OTT and Streaming apps saw a 31% increase in paid installs on Android and a striking 640% increase on iOS, suggesting that while Android drives volume, iOS continues to attract high-value users in premium content categories.

These shifts underline a growing divergence in platform dynamics. Android is increasingly associated with rapid user growth and scale, while iOS is delivering more concentrated gains in categories where users demonstrate a higher willingness to pay. For marketers, this reinforces the need to tailor acquisition strategies not just by category, but by platform, aligning spend with where conversion potential is strongest.

The report also points to significant differences in how effectively subscription apps convert users, particularly when it comes to free trials. Gaming apps continue to attract the highest share of trial users, with 12.2% of users entering free trials, but conversion remains relatively low, with only 19% going on to pay. In contrast, Education and Lifestyle apps convert more than 40% of trial users, indicating that these categories are more successful at demonstrating value within a limited timeframe. Health and Fitness apps stand apart, with many users opting to pay upfront without a trial, reflecting stronger purchase intent from the outset. These variations suggest that free trials are not a one-size-fits-all strategy, but rather a tactical lever that must be carefully aligned to category dynamics and user expectations.

At the same time, the way consumers pay for apps continues to diverge across categories. OTT and Live Streaming apps are consolidating around subscription-led models, as users commit to ongoing access to premium content. In contrast, Short Drama is beginning to incorporate ad-supported elements, reflecting a growing preference among users in fast-growing markets to trade time and attention for access rather than pay directly. This hybridisation of monetisation models is enabling developers to broaden their addressable audience while still capturing revenue from engaged users.

“The subscription app market is still growing, but the centre of gravity has shifted,” said Sarah Maina, Regional Manager, Middle East & France, at AppsFlyer. “Android is now the primary growth engine, emerging markets are driving the bulk of new subscribers, and the categories pulling ahead are the ones that figured out where their audience actually is, not where the industry assumed it would be. The marketers who close that gap fastest will have a meaningful advantage.”

Leave a comment